In this video, certified FE trainer Hilda Thuo explains how the ILO module on financial education has helped develop the resilience of refugee- and host community-led small businesses in Kakuma, Kenya.

Hilda Thuo, Livelihoods Officer with the Lutheran World Federation (LWF) and a certified financial education trainer, really appreciates the participatory approach of the ILO module on financial education and finds it highly effective at engaging participants. She is now a strong advocate for promoting financial education and wants to reach out to more business people in the community. The LWF has incorporated financial education into all its livelihood support interventions in Kakuma, Kenya and so far has trained 180 people from refugee and host communities using the ILO's financial education module.

This video showcases the success of the ILO in empowering Iraqi women entrepreneurs by providing them with essential skills and financial support, transforming their lives and creating a ripple effect of opportunity and resilience across communities.

Women in the Mina region of Iraq face significant socio-economic challenges, including systemic barriers to entering the labour market, with only one in ten participating – one of the lowest rates globally. To address this, the ILO partnered with the Lutheran World Federation in northern Iraq, providing more than 1,200 young women there with skills in finance, business management and social cohesion to support enterprise development in more inclusive communities. In addition, the ILO, in collaboration with the Central Bank of Iraq, introduced a tailored financial product used by more than 300 female entrepreneurs, addressing challenges such as training, Sharia compliance and seasonal repayment. These efforts have enabled women to become role models in their communities, with some of them training and employing younger women, creating opportunities and driving long-term social change.

PROSPECTS Iraq successfully enabled financial inclusion for MSMEs run by IDPs and host community members through an innovative loan product and adapted financial training for Central Bank of Iraq (CBI) and commercial bank staff.

Iraq has a history of instability, tied to internal and external geopolitics. As a result of the Gulf and Iraq wars, and subsequent waves of violence, large numbers of IDPs and waves of returnees have characterized much of the displacement context. Unlike other countries in the region, in Iraq the number of refugees is relatively small. Many of the areas with large numbers of returnees suffer from weak infrastructure and labour markets. Iraq’s economy remains dependent on the oil sector, with limited private sector opportunities. Entrepreneurship is also underdeveloped and the use of financial services to start and expand small businesses is extremely limited. However, in recent years, the Government has tried to support the development of MSMEs, partly in an effort to diversify the economy away from the oil sector and realize job-creation potential at the local level.

The national One Trillion Initiative was launched in 2016, whereby private banks were invited to service MSMEs with loans. Under the initiative, the Central Bank of Iraq (CBI) would advance the loan amount at a very low interest rate to encourage participating banks. However, the weakness of the financial sector, with its history of collapse, limited the initial impact, as entrepreneurs were reluctant to take on loans and commercial banks saw the potential client group as high risk, because it lacked the required collateral/guarantees. Consequently, the banks maintained unaffordable and inflexible guarantee requirements.

At the outset of PROSPECTS, the ILO launched an assessment of the demand for and supply of financial products in Iraq. The assessment revealed a weak ecosystem of enterprise support and rampant misperceptions on the part of FSPs vis-à-vis MSMEs, and vice versa. The programme therefore focused on strengthening networks of FSPs that were willing to adapt and extend services to refugees, IDPs, returnees and host community entrepreneurs and, subsequently, building their capacity to work with this client group.

PROSPECTS Iraq adapted the Making Finance Work for Refugees, Displaced and Host Communities (MFWR) course and rolled it out with staff of the CBI, ICBG, MFIs and commercial banks. It also invited staff to FE training with groups of refugees, IDPs, returnees and host community members. In some instances, commercial banks and credit agents became FE trainers themselves. This was also a measure to support the continued application of FE within nationally based institutions by enhancing understanding of the target groups’ needs.

PROSPECTS Iraq worked with FSPs to develop a wider network of enterprise support, encompassing the Ministry of Youth and Sport (MOYS), the Ministry of Labour and Social Affairs (MOLSA), business associations, chambers of commerce and chambers of industry. MOYS youth centres and MOLSA TVET centres were used as training spaces, and staff served as trainers for both SIYB and FE. This helped link financial services offered by the FSPs to other forms of BDS support. The programme also institutionalized the tool within a youth volunteer organization that was affiliated to MOYS.

In partnership with the CBI, ICBG and three commercial banks, PROSPECTS Iraq co-designed an MSME-specific loan product, including an innovative guarantee mechanism. Operationalizing the loan product took considerable time between the initial signing of a memorandum of understanding with the Central Bank (in December 2019) and the issuing of the first loan (March 2022). This was largely the result of having to clarify and modify banking procedures, and shift perceptions within FSPs towards serving IDP and host community MSMEs. Some of the more time-consuming, but critical, steps in creating the loan product included the following: Standard Operating Procedures (SOPs) were co-designed for FSPs to serve MSMEs run by IDPs and host community members. These cover, for example, reduced length of loan disbursement, seasonal repayment schedules that accommodated repayment by agricultural MSMEs, and compliance with Sharia law. The SOPs were agreed by the CBI, ICBG, ILO and participating commercial banks. They also serve as a reference point for other agencies and banks lending to MSMEs in the country. A new approach to MSME lending was co-designed, eliminating the need for personal guarantees from entrepreneurs by introducing a guarantee fund co-financed by the ILO and the ICBG. This innovative model established a savings fund, covering 35 per cent of the loan amount, which functioned as both a guarantee and a savings deposit. If the loan was fully repaid, this 35 per cent was awarded to the entrepreneur as savings. The remaining 65 per cent of the loan was guaranteed by the ICBG. By securing 100 per cent of the loan amount, the fund reduced the financial risk to commercial banks, facilitating their entry into lending to lower-income and IDP clients. Additionally, the 35-per-cent repayment reward encouraged entrepreneurs to practise responsible financial management, reinforcing their commitment to sound financial practices.

By design, partner banks were required to have a portfolio that comprised at least 30 per cent women and 40 per cent IDPs. At the time, refugees were not able to access funds under the national One Trillion Initiative, but they did have access to similar loan products through microfinance institutions with which the programme worked. As a measure of progress, after IDPs were included in the Initiative, the Central Bank asked the ILO to make a formal request to it to include refugees also, thus opening the topic up for discussion within the CBI. However, KYC requirements remained a barrier, as there was no other solution to identify and screen customers in Federal Iraq and the Kurdistan region. A further complication was the fact that Federal Iraq and the Kurdistan region have different definitions and processes for registering refugees, meaning that a refugee in one may not be recognized as such in the other.

The partnerships with the Central Bank of Iraq demonstrated that entrepreneurs traditionally left outside the banking system can all prove to be reliable when given the opportunity to access financial markets. Repayment rates among refugee, IDP and host community clients were in excess of 99 per cent, with rates among IDPs and refugees equating to those of host community clients. The intervention also shed light on the need to increase institutional and operational capacities of the private banking sector to serve refugee and host community entrepreneurs. This would include investment in dedicated staff, effective and efficient credit assessments, and enhanced customer services.

In the case of Iraq, transforming the financial sector to be more inclusive required both time and commitment to engage with both FSPs and entrepreneurs. On the side of FSPs, a clear and shared objective was required, together with the flexibility to customize and develop products suitable to the context. The ILO financial and non-financial training tools, once adapted, became part of an ecosystem of support for MSME growth and development. The model that was developed in Iraq supported the mobilization of resources in the country from other donor-funded projects, all of which aimed to strengthen access to financial systems among MSMEs.

Amid Lebanon's financial crisis, PROSPECTS partnered with Al Majmoua to offer a blended finance approach for farmers and agri-food producers, demonstrating that, even in crisis, opportunities for business growth can emerge.

At the time PROSPECTS was launched, in 2019, Lebanon had undergone a deep financial and economic crisis. Soon after the programme commenced, the situation in the country worsened, with the onset of the COVID-19 pandemic, the Beirut explosion, large and unmanaged forest fires, and widespread social unrest. The financial sector was largely insolvent and in desperate need of reform, as evidenced by triple-digit inflation and the loss of 98 per cent of the currency’s value. In the early years of programming, PROSPECTS Lebanon did not work on system strengthening or engage with formal financial systems, largely because these had collapsed. In 2022, a window of opportunity opened as the market started showing some signs of stability, partly as a result of “dollarizing” the economy. Despite this, MSMEs still struggled to stay afloat and, without a stable financial service provider to serve them, they were increasingly cash-strapped. The programme took a sectoral approach and partnered with an MFI, Al Majmoua, to develop a blended finance approach for farmers and agri-food processors. This approach challenged the predominant subsidy model in the country and took the opportunity to reinvest in the microfinance sector, which had also become largely insolvent in the wake of the multiple crises.

Al Majmoua is a pioneer in the Lebanese microfinance sector. From its founding in 1997, it focused on developing affordable financial services for micro-entrepreneurs. Even amid the multiple crises, it maintained operations and issued loan products, one of the very few institutions that was able to do so. PROSPECTS partnered with Al Majmoua, given its history and knowledge of the microfinance sector.

Following a rapid market assessment, the programme team and Al Majmoua developed a financial inclusion product for the agriculture sector. Recognizing the diversity of potential clients in the sector, three types of farmers and agriculture-related businesses were defined to better target products and technical assistance:

Microscale farmers and agri-food processors: primarily self-employed, relying on family members as daily workers during peak seasons; usually own or rent between two and four donums (a third of an acre) of land; and generally farm to supplement another main source of income. Loans for these farmers usually amount to less than US$1,500, owing to their limited repayment capacity and because the loans are primarily to help sustain their business. Syrian refugees largely fell into this category.

Small-scale farmers: bigger farms and likely to plant two seasons per year; generally hold more assets and are better established in the market; employ few fixed-term workers and take on larger numbers of workers (between five and twenty) during peak seasons. These farmers are usually served with bigger loans (US$2000–7000) and can afford to repay larger monthly instalments. Usually, the loans are used for investment in land or acquiring new technology or machinery.

Medium-scale farmers: well-established farmers with considerable land (50–500 donums), the majority of which is owned rather than rented; usually employ larger numbers of fixed-term workers; can easily afford to repay either monthly or seasonally. Loans are primarily used for expanding farms, creating jobs, or introducing new green practices. Loans are not the only type of finance used by this group.

The microfinance sector’s high interest rates were partially subsidized by the programme, as a measure to help farmers and processors, particularly micro and small-scale operators, enter the formal financial system. The product incorporated both financial and non-financial BDS, making use of the ILO Improve your Agri-Business (IYAB) training to help farmers and agri-food processors maintain or expand operations.

Loans were disbursed to microbusinesses and farms largely in the form of small, regular amounts, to allow for incremental growth. The MFI also preferred this method, as it limited its losses in the event of non-repayment. Market fluctuations at the time of the intervention (2023–24) were a challenge to its already tight profit margins and rising operational expenses.

Medium-scale farmers’ financial requirements to scale up their already large operations exceeded the capacity of the MFI, particularly as the financial sector introduced liquidity constraints at the time. Small-scale farmers and businesses were therefore the primary group targeted for the product, based on their existing capital and opportunities to scale up through investment. Micro-scale farmers required a blended finance approach.

Loan clients invested more in their businesses, and more strategically, than grant recipients. This was due, in part, to their recognition of the need to repay the loans and thus qualify for future financing. Of those reached through the MFI product, 85 per cent reported profitability in their business.

In engaging with the microfinance sector and supporting business growth during a time of crisis, the PROSPECTS team in Lebanon saw how, even in a crisis situation, opportunities can still exist for some businesses. For instance, as the crisis took hold in the south of Lebanon, farmers and agriculture businesses in stable areas saw an upsurge in demand from domestic markets. While providing food for the population was a primary objective at the height of the crisis, small businesses along supply chains sourced from stable areas did experience a boost in business, demonstrating that the impact of the crisis is not even.

The ILO and the Association of Ethiopian Microfinance Institutions’ partnership strengthened financial inclusion and resilience for refugees and host communities through integrated financial education and microinsurance initiatives.

The Association of Ethiopian Microfinance Institutions (AEMFI), established in 1999, is a non-profit, non-governmental body promoting microfinance in Ethiopia. With a network of 52 member MFIs, the AEMFI provides a platform for knowledge exchange, advocacy, capacity-building and performance monitoring, all of which focus on delivering financial services to vulnerable communities, including refugees and host communities.

In 2021, the AEMFI and several of its member MFIs participated in the ILO training Making Finance Work for Refugees, Displaced and Host Communities. This capacity-building programme was designed to equip financial institutions with tools to serve forcibly displaced populations. The training focused on adapting financial services to the unique needs of refugees and host communities and explored strategies to address financial inclusion challenges in underserved areas. Through practical guidance and the ILO’s inclusive methodologies, the AEMFI members gained essential skills to support refugee financial inclusion, highlighting a commitment to socio-economic integration.

In parallel, the AEMFI also championed the institutionalization of financial education within its network. Through the ILO’s Financial Education Programme, member MFIs have implemented comprehensive financial literacy initiatives that help individuals and families understand essential concepts in savings, budgeting and debt management. The AEMFI has played a central role in expanding financial education through training trainers in the ILO’s FE programme, enabling the development of a robust network of national and regional trainers. By leveraging the ILO’s structured training materials, which cover core financial literacy principles and adaptive strategies for refugees and host communities, the AEMFI ensures that trainers are well-equipped to educate diverse client groups in managing their finances sustainably.

Additionally, the AEMFI and the ILO, recognizing the need for risk mitigation and financial security, collaborated to introduce microinsurance as a valuable addition to MFI service portfolios. This initiative aligned with recent regulatory changes introduced by the National Bank of Ethiopia, under which MFIs are mandated to offer microinsurance to safeguard movable assets, often pledged as collateral. Microinsurance, which is especially critical in high-risk sectors like agriculture, addresses both borrower vulnerability and lender risk.

In December 2024, the ILO and the AEMFI delivered intensive microinsurance training for Ethiopian MFI managers and independent trainers, covering the diversification of financial products, client-centric product development and best practices in risk management. This workshop, informed by the local context and international case studies, equipped participants with the knowledge to design and implement effective microinsurance solutions. By incorporating microinsurance, MFIs can better serve rural and underserved communities, enhancing the resilience of both FSPs and their clients.

This partnership between the ILO and the AEMFI exemplifies a sustainable model for the financial inclusion of refugees and host communities in Ethiopia, embedding financial education and microinsurance within the strategic framework of MFIs. The collaboration strengthens both the institutional capacity of Ethiopian MFIs to support refugee and host communities through inclusive financial services and the financial resilience of the communities they serve, promoting long-term socio-economic stability.

Lessons from the PROSPECTS Uganda-Ag-Ploutos partnership using both push and pull interventions

PROSPECTS Uganda conducted an AIMS assessment that identified challenges and opportunities in supporting sesame and cassava value chains, highlighting their potential to provide livelihoods for refugees and host communities. The assessment identified several constraints, including inconsistent and low-quality input supplies, a lack of downstream agri-dealers or agents, inadequate farming practices, inconsistent supply for aggregation, poor post-harvest handling and limited market access. In response, the project began identifying private sector partners with the capacity and commercial incentive to engage with farmers in these underserved areas. Through an open call, Ag-Ploutos was selected as a partner.

Ag-Ploutos is an agricultural company that specializes in strengthening food supply chains by collaborating with public and commercial entities, including governments, cooperatives and farmers. Through its agent network it provides aggregators with quality inputs, extension services, financing, crop insurance and access to credible markets. The company had already identified a business opportunity in expanding its reach to 30,000 farmers in new territories and had already planned to expand into the West Nile region to increase its pool of quality sesame suppliers for high-end export markets. As the company’s manager explained to the programme team, it would have eventually expanded into West Nile with or without PROSPECTS’ support; however, the opportunity to work together substantially accelerated its penetration of the local market, enabling it to achieve its expansion goal in just one year instead of three. This also demonstrated that the business case was sound and aligned to the company’s own objectives.

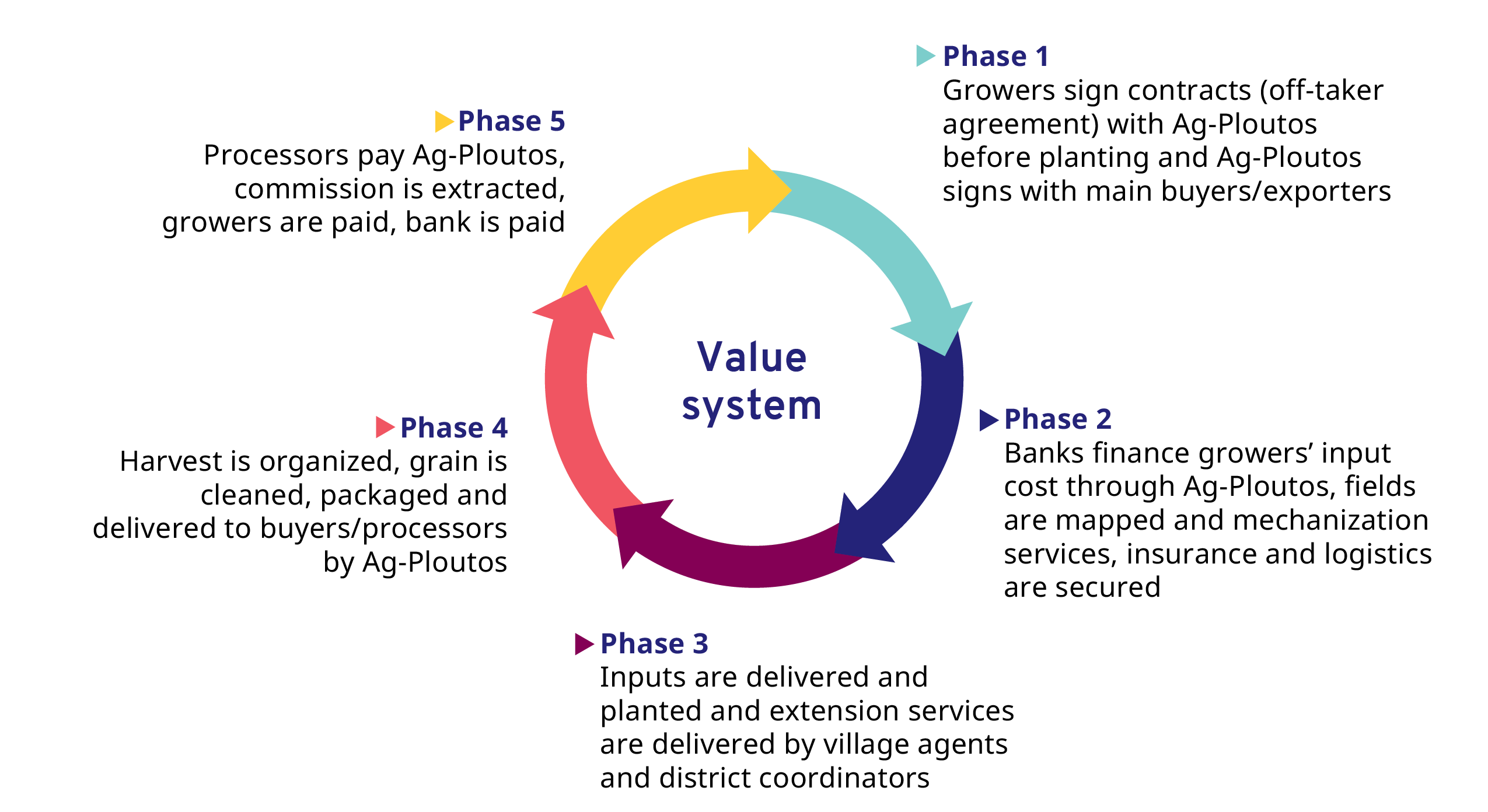

The model that was developed with Ag-Ploutus can be broken down into five phases. The graphic above illustrates these and clearly shows how the partnership facilitated access to export markets by de-risking transactions between large export buyers, banks and small-scale farmers. The phases were as follows: 1) the grower signs contracts with Ag-Ploutos, which, in turn, signs contracts with export buyers; 2) based on the guarantee provided by these contracts, local banks agree to finance growers’ input costs through Ag-Ploutos, which will recover the loan on behalf of the bank. At the same time, fields are mapped and mechanization services, insurance and logistics are secured for the growers; 3) inputs are delivered and planted, and extension services are implemented through a network of trained village agents and district coordinators; 4) village agents buy back the sesame production from farmers, deducting a pre-financing cost of the inputs from the total. Ag-Ploutos aggregates the sesame harvest locally and has it cleaned, tested and packaged in Kampala; 5) export buyers pay Ag-Ploutos, a 5% commission is extracted for the village agents and the loan to the banks is paid back.

Alongside the extension services, the programme team facilitated training with the National Organization of Trade Unions to train farmers in occupational safety and health. This addressed decent-work deficits observed at the farm level and served to support compliance with export buyers’ requirements.

Because the farmers involved were small-scale and largely unregistered, Ag-Ploutos also developed a digital profiling tool for the farmers, accompanied by an evaluation tool. The profiling tool provided basic information about the farm, such as crops grown and geographical area of operations. The evaluation tool allowed farmers to receive ratings from buyers, which helped legitimize their operations. The evaluation tool was also expanded to predict productivity potential of the farms and evaluate compliance with labour standards. The two tools were adopted by banks for the purpose of due diligence, which also helped previously unbanked farmers access finance.

Results:

In all, 5,740 refugees and host community farmers had access to inputs and extension services, as well as guaranteed access to export markets.

In one season, 350 tons of sesame worth US$420,000 were produced and aggregated.

The new seed variety introduced by Ag-Ploutos improved farmers' yields, increasing them from 100 kilograms per acre to 500 kilograms.

Farmers’ revenue increased by a minimum of 150,000 Ugandan shillings (US$40) and up to 800,000 shillings (US$216) in one season.

In total, 890 individual bank accounts were opened for farmers at Equity Bank.

Overall, 215 businesses were started in the sesame value chain.

Find out more about this project in these reports: